Pension offsetting in divorce

Sounds simple. Often isn’t. Expert analysis to support confident offsetting decisions.

What is Pension Offsetting?

Pension offsetting in divorce is where one party keeps more of the pensions, while the other receives a greater share of other assets.

Rather than dividing the pension through a Pension Sharing Order (PSO), offsetting balances the value of the pension against other marital assets, like a property, cash savings or investments.

It sounds simple. But pensions are difficult to value accurately and even harder to compare fairly against other assets, making it easy to agree an offset which is unintentionally unfair.

73 years

collective experience

1 goal

to simplify complexity

5 specialists

with technical expertise

10 days

from data receipt to report

When is pension offsetting appropriate?

Pension offsetting in divorce is appropriate when:

There is a strong desire to retain the family home

A clean break is preferred

One party places greater value on retaining a specific asset now than receiving pension income later

But because pensions are difficult to value accurately, without proper modelling, it can be very hard to know whether a proposed offset is fair.

62%

62% of clients consider pension offsetting

And that’s not surprising. People commonly offset pensions against property.

Property feels tangible and emotionally important. The desire for stability and a sense of ‘home’ after divorce can be powerful.

Trading pension value for property can be the right call. Just make sure the differences are fully understood before decisions are made.

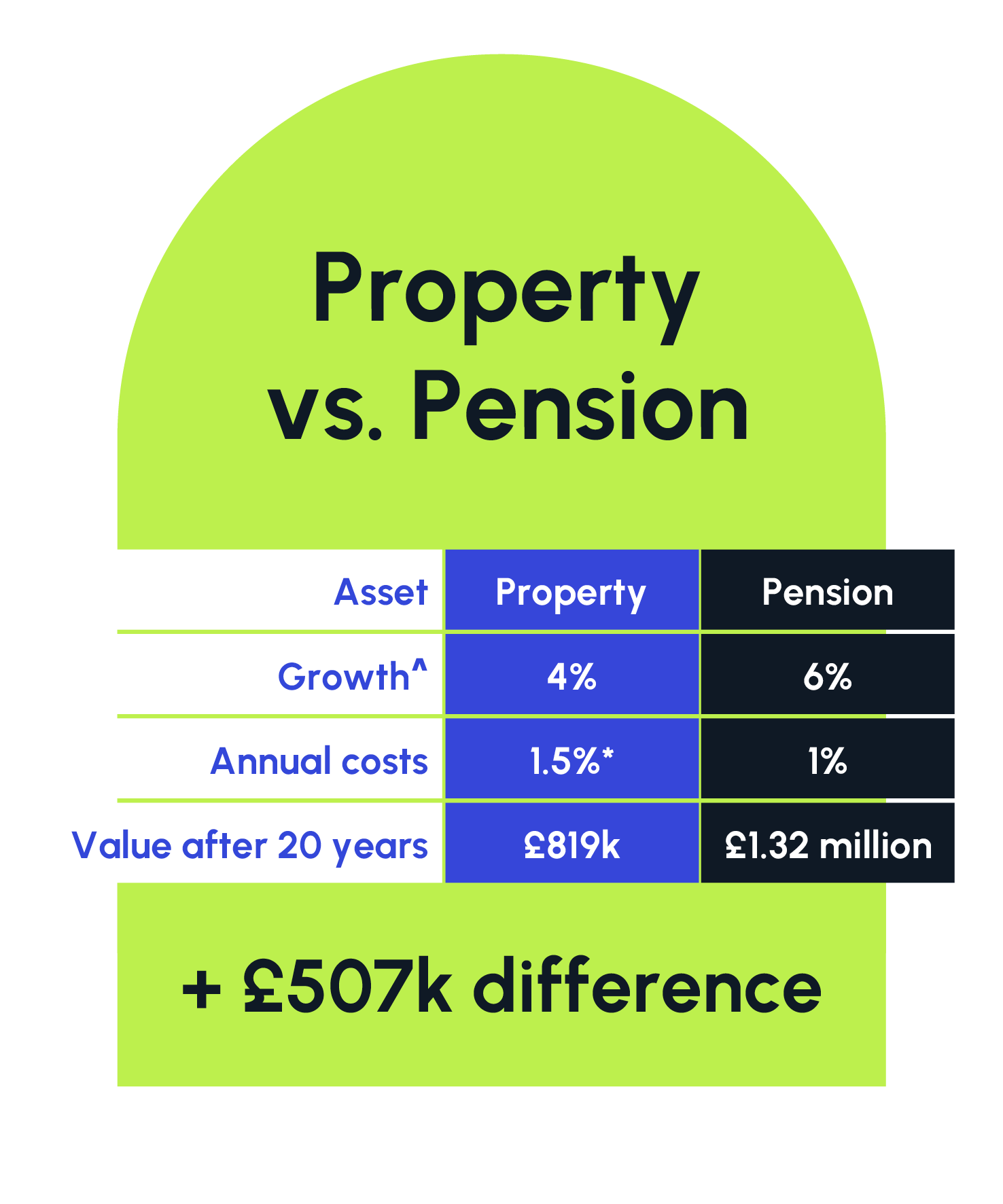

500k pension and 500k equity do NOT have the same value

Pensions are most commonly offset against property. But they are completely different types of asset.

Property = Immediate value + flexibility + no retirement restrictions

Pension = Future taxable income + long-term security + scheme benefits

This is why offsetting requires careful modelling rather than simple comparison.

Should I consider Pension Offsetting?

Why using CEVs for pension offsetting is risky

Many people use Cash Equivalent Values (CEVs) to work out what pensions are worth to inform the offset value. But CEV’s don’t tell the full story.

Some CEVs overstate value, so you give away more than needed

Others understate value, so you end up with less than you’re entitled to

They also ignore income potential, survivor benefits, and scheme guarantees which are highly valuable and difficult to value

Dividing pensions or offsetting with a CEV would be similar to valuing your house with Zoopla. A PODE report provides a more detailed and reliable assessment of pension value, so offsetting decisions are fully informed.

Where’s your Pension Offset calculator?

Many people search for a "pension offsetting calculator" hoping for a simple answer. There are online calculators available, but they often rely on overly simplified assumptions.

Real-world offsetting decisions involve factors such as tax, pension type, retirement age, inflation, property equity and personal priorities. A fair outcome rarely comes from a simple formula.

Pension offsetting is far more nuanced than most calculators can accurately reflect, which is why we don't have one.

More about pensions on divorce

-

Pension Offsetting on divorce. Why it's not as simple as it looks.

-

How do I talk to the other party about pensions on divorce?

-

What's PAG and why does it matter for my divorce?

Frequently Asked Questions

-

Pension sharing divides the pension itself, so each party has their own separate pension pot moving forward.

Pension offsetting in divorce means one person keeps more of the pension while the other receives more of a different asset, such as property or savings.

Offsetting can be a good option but it’s important to accurately value the pension to inform the offset value and to understand the long-term impact before agreeing.

-

Once all pension information has been received from providers, our reports are prepared within 10 working days.

The main variable which affects overall time frames, is how quickly pension providers supply information we require. We’re not in direct control of this, but have rigorous processes in place to chase providers and ensure they provide the information we need as quickly as possible (read more).

-

Quite the opposite.

Expert clarity often reduces conflict and speeds up agreement because both parties are working from the same evidence-based analysis.

-

We have fixed fees so that you can predict and manage costs. We do NOT charge for extra calculations.

Costs vary by report type (get the run down on costs here)